Corporate Deals Drive U.S. Oil & Gas M&A To 4-Year Record Before Year-End Stall

$84B in 2018 highest since $101B in 2014

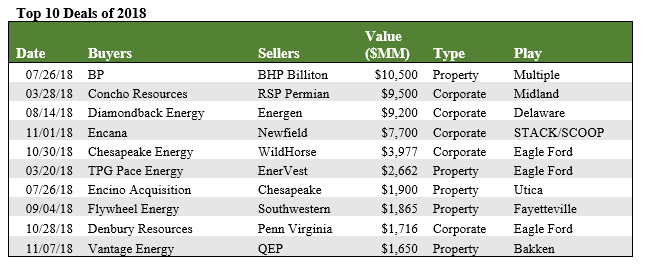

Drillinginfo, the leading energy SaaS and data analytics company, announces that U.S. upstream oil & gas M&A clocked in at $84B in 2018 for the highest total since oil prices fell from their peak in late 2014. Large billion dollar plus deals fueled the surge in the back half of the year with a record-setting $32B in 3Q18 and $21B in 4Q18. BP’s transformational $10.5B buy of most of BHP’s shale assets is the largest deal of the year and fourth largest since 2009. The deal underpins BP’s strategy to roll-out BPX as an independent and leading US shale player. The year also ran a close tie with 2014 for the most public company consolidations with RSP Permian, Energen, Newfield, WildHorse and Penn Virginia leading the exit list in 2018.

As Drillinginfo predicted in July 2018 the pace of consolidation picked up late in 2018 with corporate-level deals accounting for over 70% of the $21B total deal value in 4Q18. That is the highest quarterly corporate deal total since 3Q14.

“Investors continue to demand that companies deliver a clear line-of-sight to positive free cash flow,” said Drillinginfo M&A Analyst Andrew Dittmar. “Scale is one piece of the puzzle on how to get there given efficiencies in developing larger acreage blocks, optimizing supply chain logistics to lower costs and G&A savings. Wall Street no longer supports growth for growth sakes and is ready to punish buyers who do deals without a clear profit strategy."

With the precipitous drop in oil prices that broke all support levels beginning in early November, the deal markets ground to a virtual stall. This came almost immediately on the heels of perhaps the most talked about week in the industry’s recent history. In a span of just five days, public company consolidation went into a frenzy with Denbury buying Penn Virginia, then Chesapeake buying WildHorse and Encana purchasing Newfield.

The shift towards corporate-level M&A late in 2018 also cut into private equities’ share of deal activity. After hitting a high-water mark in 4Q17 by taking the buyer role in 46% of deals, private equity’s share of acquisitions fell to only 7% in 4Q18. Private equity wasn’t overly active as a seller in 4Q18 either, accounting for only 4% of sold deals by value versus 23% in 4Q17.

Another clear theme from 2018 was the institutionalization of the minerals market with deal activity in this sector growing 100% over 2017 with deal value reaching nearly $3B. Buyers cross all capital sectors from public royalty companies like Kimbell Royalty Partners to institutional players like Ontario Teachers’ Pension Plan to public E&Ps like Continental Resources.

Looking forward into 2019, Drillinginfo expects the pace of oil and gas deal markets to remain impacted by oil price volatility which ultimately provides numerous special situation opportunities, particularly for oil equities that have been oversold. According to Brian Lidsky, Sr. Director Market Intelligence, "The straight-line $31 drop in WTI spot oil prices from $76 to $45 per barrel from the start of October to just before Christmas coincided with the risk-off appetite that was pervasive across the capital markets. US E&P equities responded largely in lock-step with the rapid decline. Looking ahead, the reality is that albeit global oil demand may slow some, growth remains unabated and for all intents and purposes has surpassed the 100 million barrel per day level. All eyes are on the impact of the start of OPEC+ round two cuts, Iran sanctions plus the trend of global oil demand.”

Currently, Drillinginfo quantifies $39B of deals in play in the U.S., of which 50% is located in the Permian. There is certainly high-quality assets in the marketplace and buyers ready to acquire. The only barrier is bridging the bid/ask price. Historically, if the gap has widened, deals often come with contingent payments predicated on a price or asset performance benchmark.

Top Takeaways from 2018:

- Total of $84.3B in 2018 with $20.9B in 4Q18 and 63% of total value in 2H18.

- For 2018, Permian is again most active area for deals with $28.3 B or 33% of total.

- Funding asset acquisitions via an overnight equity raise became virtually non-existent.

- SPAC business model (raise public market cash then find an asset) continues to work.

- The IPO market for E&Ps remains largely closed.

- Royalty markets double and rapidly gain institutional attention.

Outlook for 2019:

- Expect the launch of numerous non-core asset sales from public E&Ps with BP likely leading the charge.

- Private equity likely to reemerge as a key buyer on asset deals with willingness to pay for PDP and take risk on upside.

- Markets will reward scale and low-cost leaders which translates into richer equity currency for large players to make accretive buys of smaller players.

- Remains to be seen if rapid drop in oil prices will affect the closing of 4Q18’s corporate deals.

- Leveraged E&Ps likely to find themselves under renewed pressure to take action to improve balance sheets.

About Drillinginfo

Drillinginfo delivers business-critical insights to the energy, power, and commodities markets. Its state-of-the-art SaaS platform offers sophisticated technology, powerful analytics, and industry-leading data. Drillinginfo’s solutions deliver value across upstream, midstream and downstream markets, empowering exploration and production (E&P), oilfield services, midstream, utilities, trading and risk, and capital markets companies to be more collaborative, efficient, and competitive. Drillinginfo delivers actionable intelligence over mobile, web, and desktop to analyze and reduce risk, conduct competitive benchmarking, and uncover market insights. Drillinginfo serves over 5,000 companies globally from its Austin, Texas, headquarters and has more than 1,000 employees. For more information visit drillinginfo.com.

Source: Drillinginfo